Interesting Interest Rates

Finance & Society

This piece is a tidbit focusing on market possibilities that western countries have not seen for a generation or longer. Personally, I simply thought interest rates would never be lifted in my lifetime and asset values would continue toward the sky as long as I could look up, and yet that which could not persist finally did not persist. As well we will now all pay only as early as we were forced for our collective ignorance.

The short run now looks bad, the medium term catastrophic and for whomever of us is left the long run will likely return a cycle of growth and expansion from contractions we are currently initiating.

For decades the financial industry has been selling a narrative about the return from long term investments in the market. The government has joined that chorus and added assurance of their ability to manage all liquidity crises and debt cycles with monetary policy. They will deliver liquidity when the market cannot or so the thinking goes and we the people have demanded easy but false answers to our porblems. I belive we have no look far enough back or wide enough around for alternative possibilities.

In short, our leaders suggest they have it all under control while we bury our heads and believe eveything will be ok.

ZIRP (Zero Interest Rate Policy)

Low interest rates make everything seem like it’s better than it can sustain and not knowing any better we have been duped by false signals. The Fed and politicians in favor of ZIRP have ignored or are unaware of the costs of such and the future hell they will always imply.

If I relate interest rates to their fundamental source: trust, we get a litte more perspective. There are some amount of criminals in society and yet, we do not want to be fully closed to others, implying very high even infinite interest rates. Neither do we want to be nice and skeptical (Zero interest rates) to the point that we become prey to the worst people and the worst kinds of coercion.

ZIRP from my point of view is akin to asking the devil to dinner, because he swears if invited it will be a grand feast. Without our hackles raised we assume we have a shared concept of whom will be eating and uopn what. Our long but limited expereince has led us to unknowingly become turkeys who are charmed by our socio-political benefactors.

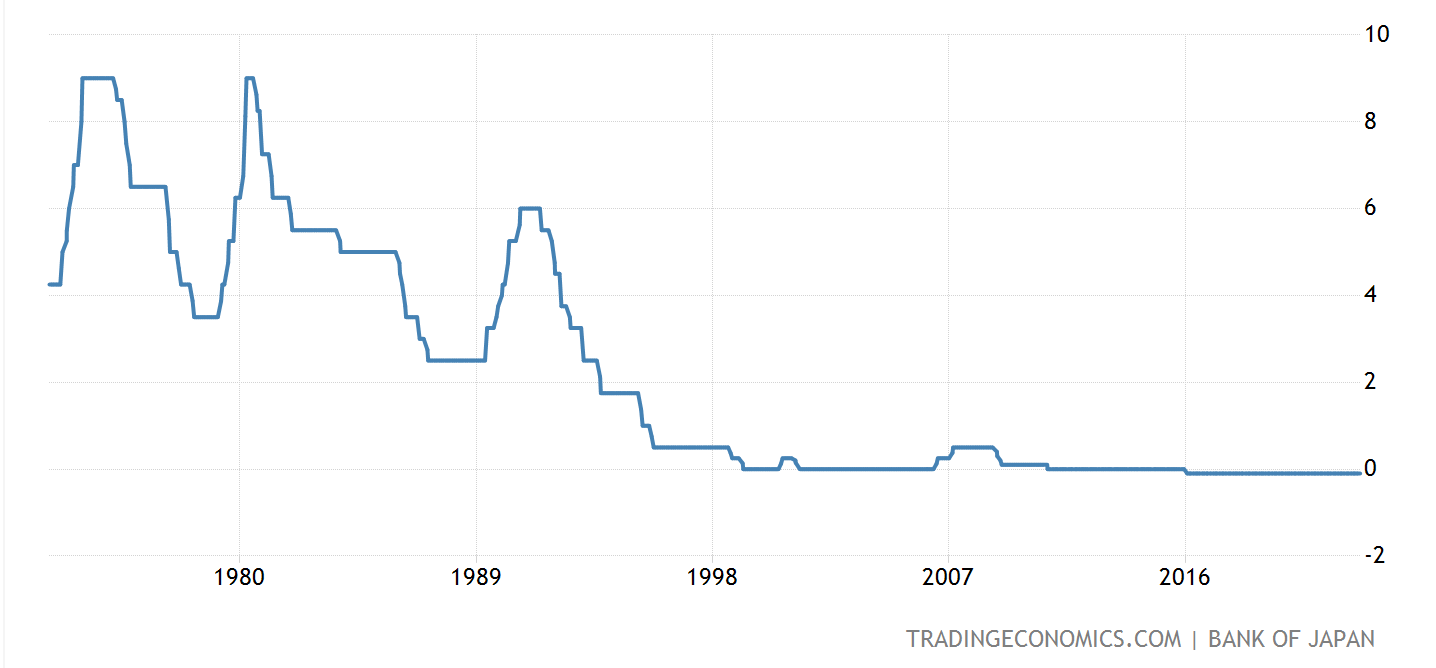

Exemplary Japan

Very few people outside of finance seem to know that policies in the US (and thus 70+% of the globe) have lagged Japan by a decade or two. They went to zero interest rate policy (ZIRP) faster and harder than any other nation from a peaks in 1981 and 1990. Here are the interest rates set by the Bank of Japan (BOJ) over the last five decades:

Japan marched towards their zero interest rate starting in the early 1980s and within a decade they created one of the world's largest asset bubbles in both housing and financial assets. A massive bubble in housing and financial assets...does that sound familiar?

Both of those markets peaked and then popped from around 1990 - 1991. The Nikkei can be thought of as the Japanese equivalent to the S&P 500. Below is the Nikkei price level over time with data from left to right moving us towards the present.

Notice that the Nikkei has trended negative from January 1990. This is a famous financial bubble pop coincident with a policy rate hike from 2 - 6%. Through 1992 the market was down about 50% and then continued down another 50% of the remaining value over the years 1992 to 2010. From 1990 the Bank of Japan lowered rates from 6% to 0% over 5 years, but the market did not return.

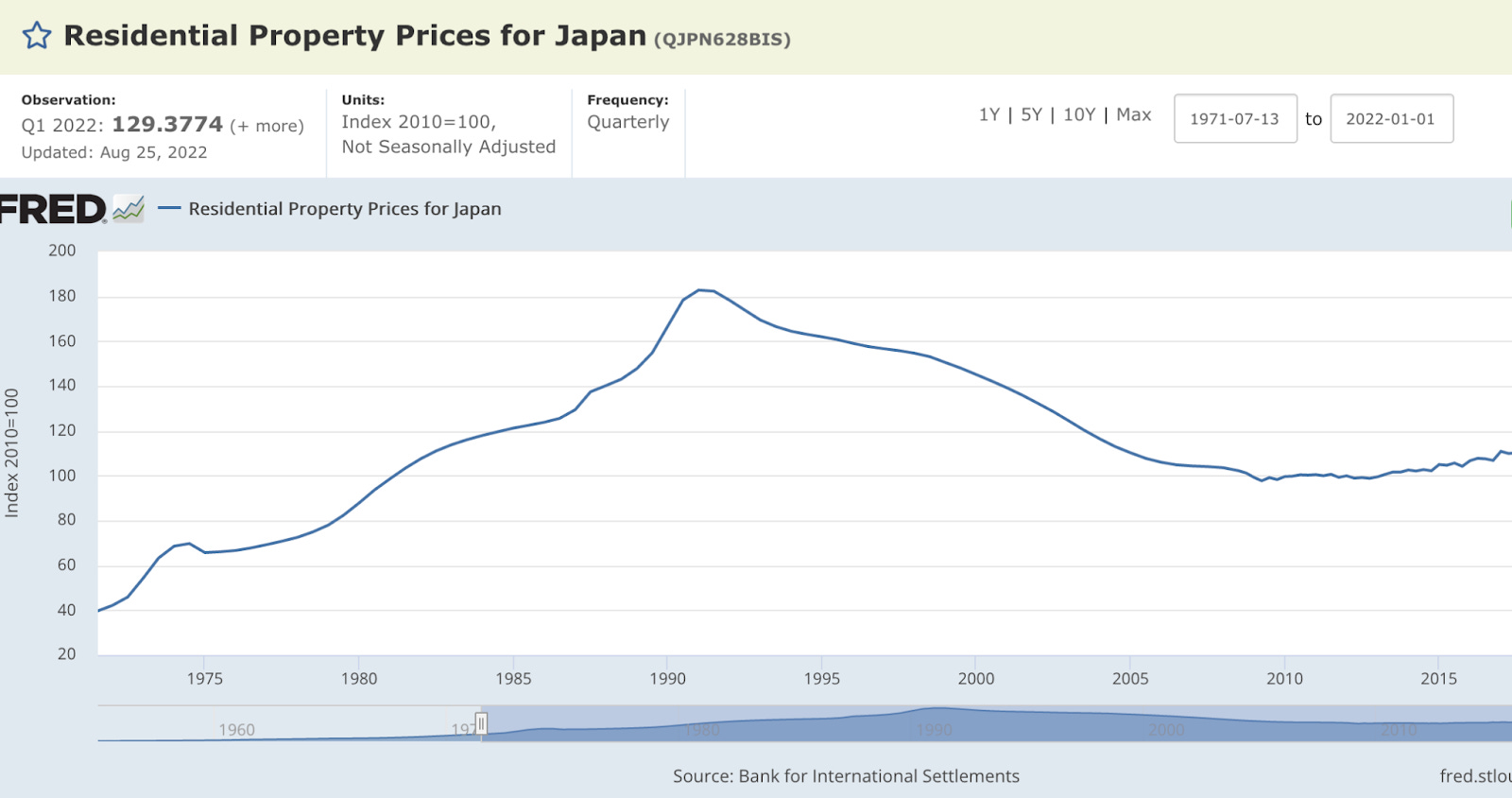

Similarly but slower the real estate market also cratered for most of that time:

Notice that the real estate market took a few months to years to begin its much slower but similar magnitude decline. The median home price halved over the 17 years from 1993. Despite effectively zero interest rates from 1998 onward the market never rallied during that period.

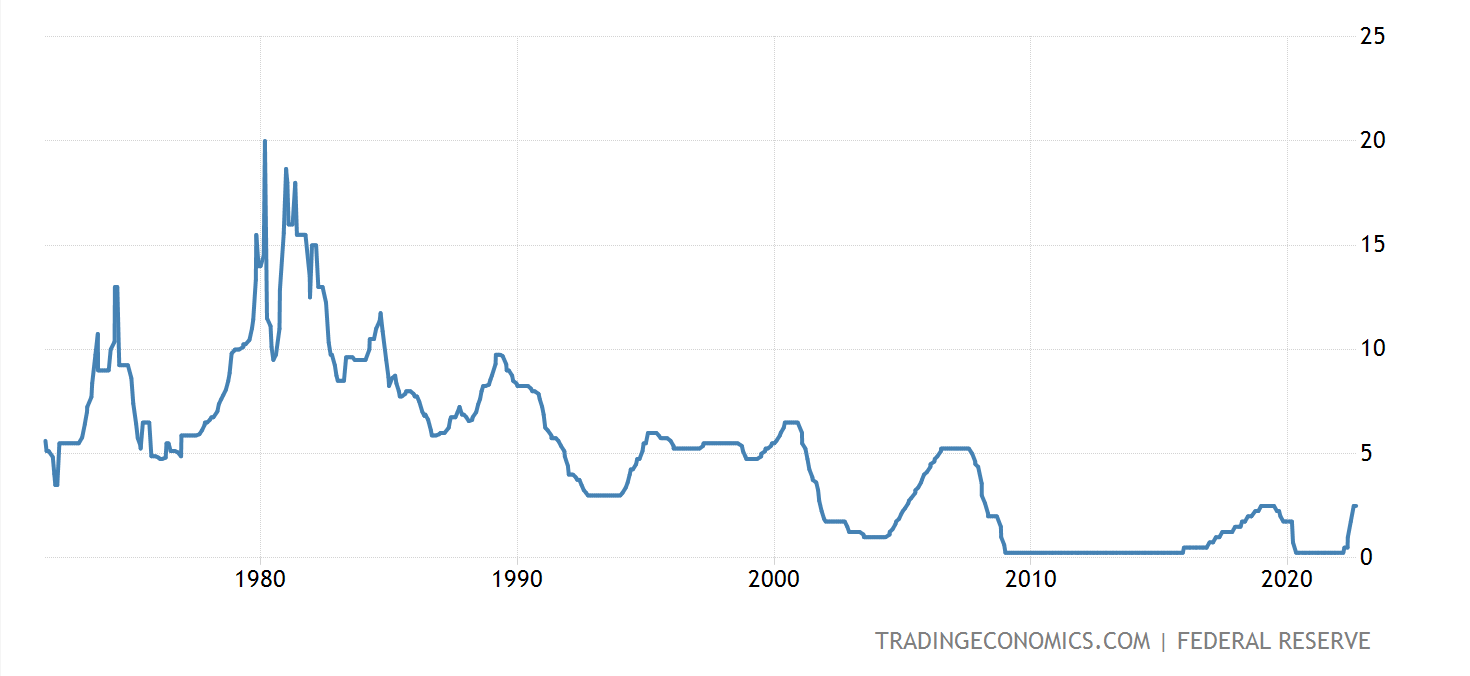

Policy Mimicry

Below are US interest rates over recent decades. We can see that we toyed with ZIRP for the first time in 2002, where we reflated the bubble in tech, pumping it into housing. Housing which inflated dramatically and then popped or fell over in 2008 after the Fed raised from essentially 1% to 5% from 2004 - 2007. This is why some people blame the Fed for the global financial crisis

...it is not an unreasonable position. In the current Fed’s defence they have only so many tools, and concencus seems to have encourage the interest rate decline.

After significant consumer price inflation from both increases in money supply and decreases in goods available, the Fed is now reversing 40 years of unidirectional policy. So far we’ve seen the S&P 500 lose about 30% over 8 months while rates have moved from 0 to 3.25 percent and the Fed promises evermore more hikes. It looks to me like the same dance. Do we think US housing might come to look like Japan?

I would bet on it.

Correlation, causation and mechanism

What I’ve shown are some loose correlations. I’m fairly confident that interest rates driven by central banks have enormously outsized effects on the regulated economies. I feel this way because the mechanism (theory) is corroborated by data ( empirical findings). It’s not certainly right, but that combination is a higher standard than much of what I typically see in both health and economics research and then all the blah blah nonsense always supporting the status quo and vested class of interests.

There are many mechanisms describing the relationship between interest rates and asset prices but we should look at two. One for each large asset category: stocks and mortgages.

Stock Valuations

Stocks are valued multiple ways and those valuations are influenced by interest rates in multiple other ways, but let’s look at 2: NPV and Corporate Finance.

NPV

Net Present Value is one of many methods to value stocks or really any asset. NPV says that the current value of an asset is equal to the future cash flows discounted by the cost of capital (the interest rate) for each period. Let’s learn from extremes. Let’s say we have 0% interest over 5 periods of paying 10 units. The NPV is simply 50. If the 0 goes to 10%; however, we have an NPV of 10/1.1 + 10/(1.1^2) + 10/(1.1)^3 + 10/(1.1)^4 +10/(1.1)^5 = 39. This is a 22% value loss from simply a raise in the interest rate aka discount rate. For most stocks this value is determined by the expected earnings per share (EPS), but something very sinister is baked into the whole stock market by incentives, policy, culture and law.

Stock Buybacks

Stock buybacks are when a company uses cash or debt to reduce the amount of shares outstanding. They simply purchase them at the market price. This is a way for CEOs to increase earnings per share, EPS, and maximize shareholder value, at least in the short run, without really increasing real earnings. Reducing the denominator (the count of shares) even makes future potential earnings increases more impactful.*

*Note that financial engineering like many costs cutting exercises fail to increase throughput. Through put is the link between physiology, business and economics. Being ignorant of the importance of metabolism or throughput we allow corporations to do the equivalent of insane weight loss. The doctor says loosing weight is healthy lop off an arm and voila better health right? Unfortunately most of the experts in most domains are obsesed with the wrong metrics and leading everyone to make absurd decisions.

Investment websites say that stock buybacks should happen when a CEO believes the market is undervaluing its stock. However, the use case is much broader, more related to the costs of capital, and much more likely to occur when valuations are already stratospheric. That is when interest rates are nearly zero.

The cost of equity capital is something like the expected earnings growth or dividend per share. If we simply think of a dividend company, one without really trying to grow, this company returns all its capital to investors. For this company both equity and debt are sources of capital for the company to operate. If debt is essentially free then a CEO is almost obligated to reduce the capital costs and increase stability of access to capital by buying back stocks. The CEO uses debt to reduce the outlay required or expected by dividends. With consistent total earnings this makes remaining stock values go up with reduced shares.

As rates have been dropping, this has been happening across the market...for decades. From the outside it’s nearly impossible to know which companies are growing from real, unbaked earnings and which from some kind of real improvements. The overall market is likewise going up, but it’s not a chart that considers the potential reductions of outstanding shares. Things seem good when the market is up...but perceptions can be quite misleading.

Imagine you are a CEO or CFO incentivised with huge stock options as part of your package and the government reduces interest rates and thus the cost of capital by a non trivial amount. For both you and the current cohort of investors you should, you must borrow as much as possible and buy-back as many shares as possible. Maximizing shareholder returns is your number one objective, and that is how you do just that. On some level what you are doing is realizing the stock value of the company by trading it to the debt risk counterparty. If you are a big company it looks like you are sound, maybe yes, but maybe that will turn out to only be true when capital is cheap. You actually sell that soundness which is in some sense just cashing out the trust of goodwill built up by the firm's history of acting reliably for owners and customers.

Systemically lowering rates bakes in a future crisis or a profound bear market. If ever rates were to return, the capital costs funded by debt would dramatically increase thus increasing the costs of capital to the firm. To reduce those costs they will either have to pay down debt or replace it with equity causing the opposite dynamic of further suppression of stock valuations.

From a theoretical perspective companies should likewise abandon all activities that (for the equivalent risk) do not pay the market rate..which if done well after a material rate hike should cause many activities to be shuttled. Many companies will even find that they should not even exist and their new realized asset values will materialize only through default and bankruptcy after their shareholders have been wiped out.

Oops! Maybe we should have made the requirement...maximize long term or full credit cycle shareholder value. Bad corporate governance and bad public policy seem to go hand in glove.

The Housing and Mortgage Markets

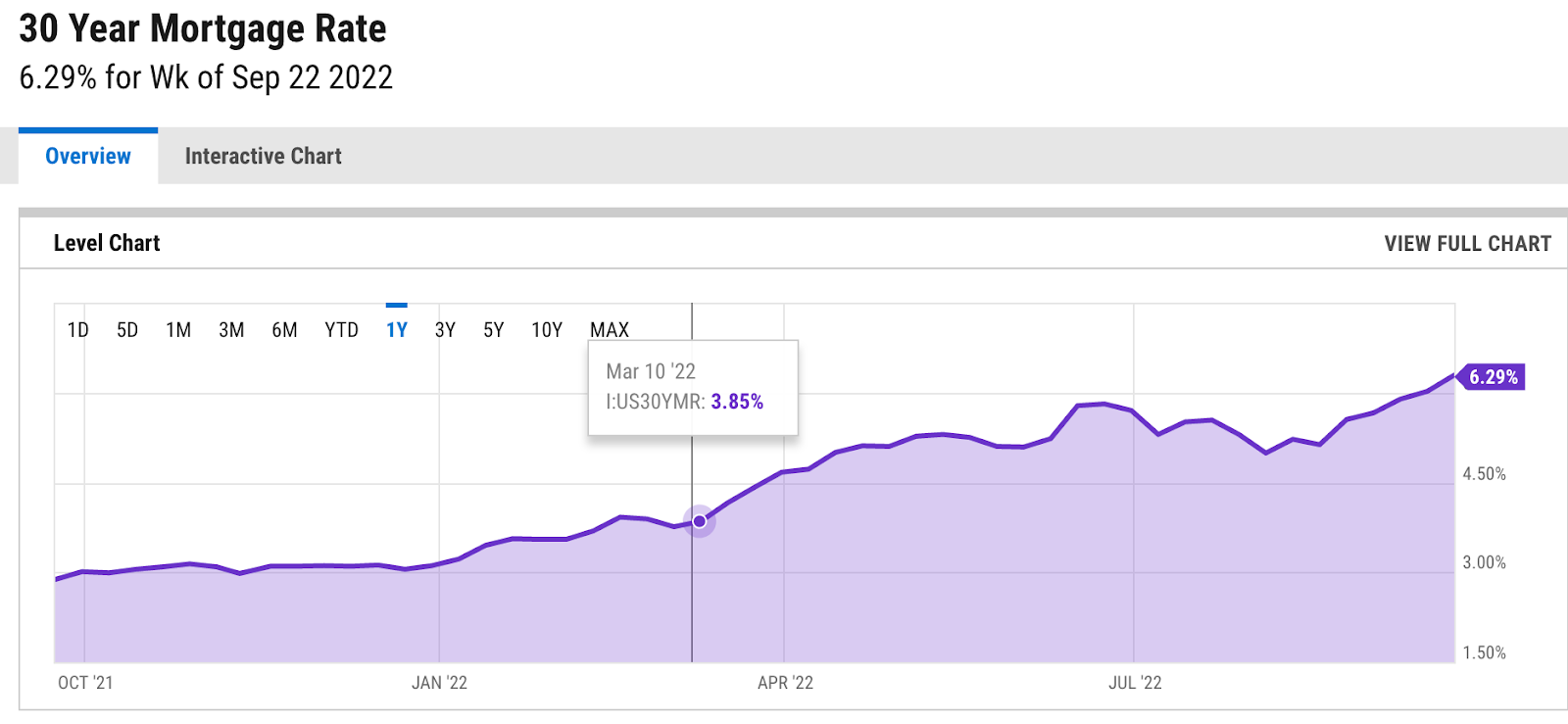

A 1,000,000 priced home bought based on 3% interest rate has equivalent monthly payments as a 680,000 home based on an 6.3% interest rate. That's a 32% change in the price based on the ability to pay monthly which is what both banks and consumers base purchases on. That reduction does not take into account the lost jobs from a massive market slowdown caused by reduced building, reduced consumption and overall recession...or depression.

We will not see housing prices reduce as fast as stocks because they are very illiquid and sellers are very hesitant to realize losses, but as the Japanese market shows. Eventually they must...little by little the housing market comes off as buyers are no longer able to access the same magnitude of mortgages.

Think down 32% is bad? Imagine you are in New Zealand where >40% of new investors mortgages and 20% of retail mortgages are interest only. Here a 1 million dollar house here and 900k mortgage can be had for only 2250 a month...which is hard to pass up when the equivalent rent is 4000 per month or more and there are no capital gains on real estate!

However, when rates go from 3 to 6.3% the monthly costs jump more than 100% to about 4700 a month (from 2250)! Whomever would potentially be purchasing from them or anyone like them in the market will no longer be able to. An equivalently qualified borrower will now only be able to qualify for a 430k mortgage when he could previously obtain a 900k mortgage!

Ipso facto: home values will need to reduce by more than 50% because interest-only mortgages are very sensitive to rate hikes. Also, IR mortages have reset periods on the front end which will force the market down relatively rapidly as existing owners simply cannot afford their resets in the near future.

Western governements have not only allowed, but have incentivised massive leveraged gambling which just happened to also benefit the sitting generation of owners.

Highly leveraged borrowers are more exposed to future increases in interest rates than others, especially as mortgage interest rates are only fixed for short periods in New Zealand - 78% of outstanding mortgages will have their interest rates reset within one year (source: OECD)

So the same generation that was forced to save to get into houses with absurd down payments on absurd valuations will now have many forced to forfeit their equity and become renters. It will take a while for many to realize that prices have stopped “always” going up.

This will include much of what is left of young men, who will have ever harder choices about how to survive such economic times.

Some simple predictions:

Each political party will try to capitalize on the stress, displacement and catastrophe

by blaming the other side

The easy but wrong answers will win public favor

Tensions will continue to mount

Crime will continue to rise

Political distances will continue to grow

Drum beats of war will beat ever louder

I can see that this is in dire need of an edit. Apologies for all who suffer through. I hope you can find the content through all the mess.

What mess other than the heart of darkness we are entering into..Phenomenal writing. Will do my best to maintain optimism.. but clearly it’s getting tougher and tougher.